Summary: Property assessment appeals have impacted the assessed values of a retail development aided by tax-increment financing (TIF). As a result, special assessments authorized by the development’s status as a Neighborhood Improvement District (NID) have been levied in the past few years. Yet again, the risks of TIF for retail have been laid bare.

“A Neighborhood Improvement District will be created by the township pursuant to the Neighborhood Improvement District Act and a special assessment will be authorized by the township and imposed on the taxable property within the TIF district… Special assessments shall be levied in any given year only if the tax increment revenues are insufficient to cover debt service on the TIF bonds, funds transferred to the public safety fund, and administrative costs related to the TIF bonds.”

-Redevelopment Authority of Allegheny County, Frazer Mills Tax Increment Financing Plan, September 2002

“Since 2016 a number of owners of property located within the TIF district have appealed the real estate tax assessments currently imposed by the local taxing bodies. … Although there has been no failure to pay any Special Assessments in the past, [the Redevelopment Authority of Allegheny County] expects that the probable reduction of TIF revenues and related increase in Special Assessments may have a material adverse effect on property owners within the TIF district and therefore, may have a material adverse effect on the ability of RAAC to repay the bonds when due.”

-Redevelopment Authority of Allegheny County, Material Event Notice to Municipal Securities Rulemaking Board, July 2018

With a few years remaining for the Pittsburgh Mills TIF district ($50 million in bonds were issued in 2004 and the district expires in 2023) assessment appeals have had a major impact on the retail development.

An examination of the assessed values of the 37 taxable parcels contained in the Neighborhood Improvement District (NID) reports for 2018, 2019 and 2020 and their recent appeal status on the Allegheny County real estate website shows 25 parcels underwent appeal while 12 did not request an appeal. Of the 25 that appealed, 12 have a lower assessed value as of 2020. Of those 12 appeals eight are currently at the Board of Viewers.

The most significant reduction was for the mall itself which is now assessed at $14.1 million, reduced from 2018’s value of $138.4 million. It sold at auction for $100 in January 2017 following a foreclosure and then was involved in a 12-parcel sale for $11.3 million in April 2018. A September 2017 news article stated the owners of the mall were seeking a 92.7 percent reduction in assessed value.

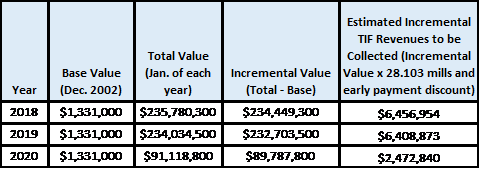

As a result of the appeals, the overall assessed value in the TIF district decreased from $235.8 million to $91.1 million. The mall’s assessed value as a share of the total assessed value of all the parcels fell from 58 percent to 15 percent.

The assessed value of the Pittsburgh Mills development accounts for nearly all of thetaxable commercial value in Frazer Township. Based on the Allegheny County assessment rolls for 2018 through 2020 the township’s taxable commercial value fell from $239.4 million to $94.7 million.

Assessed Value of Pittsburgh Mills Development, 2018-2020*

*The 2019 total value was adjusted sometime after Jan. 2019 to $91.1 million

as a result of the appeals according to Frazer Township

From 2004 to 2015, the incremental property tax revenues (taxes based on the increase in property value compared to pre-TIF development value) satisfied the requirements of servicing the TIF debt and related costs and the special NID assessment did not came into play and no annual NID payments were required.

However, since 2016, properties have been subject to the annual NID payment. In the years 2016 to 2020 total annual payments were $1.2 million, $923,000, $825,000, $5.8 million and $5.95 million. In 2020, of the 28 parcels subject to an annual payment (nine parcels of vacant land will not make an annual payment), nearly all will pay more through the NID annual payment than they would on their 2020 assessed value and current millage rates.

The 2020 NID report notes that, due to tax refunds for appeals that lowered assessments, there will be an additional NID payment for 2019 of $4.6 million ($1.2 million for 2019 was already billed), bringing the total NID assessment for 2020 to $10.6 million.

The amount outstanding on the TIF bonds after payments through July 1, 2020, will be $14.9 million. There are two interest payments and one principal payment due by July 1. After this year the annual NID special assessments in 2021 through 2023 are $6.1 million, $6.2 million and $6.1 million. These assessments, if considered to be taxes on the property, would represent a millage rate of nearly 70 mills.

Under the NID law 40 percent of the affected property owners have to object to the district for it not to be created. The 2003 ordinance noted there were no objections to the NID provisions. Presumably ownership changes in subsequent years (20 parcels have sold since 2014) have come with full knowledge and understanding of the TIF and NID being in place and what those entail.

In the 2003 NID plan it was stated that “it is reasonable to believe the owners are acting in their interest in consenting to this [NID] imposition because the benefit they receive from the public improvements exceeds the cost of the special assessments.” In light of the large payments now being made, is that still the case?

Once the TIF district expires and the bonds are fully retired, the diversion of taxes ends and all property taxes collected will go the TIF participating taxing bodies, Frazer Township, Deer Lakes School District and Allegheny County. The tax revenue will be much less than was expected if assessed values remain at current levels. Based on 2020 millage rates the difference in total property taxes generated is $4 million based on the new values after appeals.

There are 13 TIF districts in Allegheny County that are set to expire between 2024 and 2035. Based on the county’s evaluation criteria contained in its 2015 TIF guidelines there is to be “avoidance” of TIF for retail developments. Time will tell if that is adhered to.

We long ago warned about the use of TIFs for retail projects. TIFs were designed to help create good jobs-producing redevelopments in blighted areas but were quickly adopted for retail where multiplier effects are nil and where the projects become major competitors for customers of non-subsidized retail outlets.