Summary: Allegheny County is facing property assessment lawsuits. At the same time, the county’s elected officials have considered, and are considering, a number of ordinances that deal with the aspects of the assessment system. All of the ordinances stop short of mandating a specific cycle for conducting reassessments.

In February, County Council passed, and the chief executive signed, two ordinances establishing training and education requirements for the Board of Property Assessment Appeals and Review (BPAAR) members and hearing officers (in addition to qualifications already in existence) and requirements to expedite the process by which assessment appeals are heard and a decision is rendered.

In April, the council passed, and the chief executive returned, without a signature, an ordinance requiring the council’s confirmation of the chief assessment officer and for the officer to submit regular reports on assessment activities. The county’s Home Rule Charter requires that the council confirm only the county manager and the county solicitor.

In June, County Council passed and the chief executive signed an ordinance that moved the deadline for assessment appeals in non-reassessment years. For 2025 appeals the filing deadline is Oct.1, 2024. In future non-reassessment years, the filing deadline will be Sept. 1.

Part of the reasoning of making assessment appeals prospective was “to allow for increased budgetary certainty on the part of both municipalities and property owners.” The county, Pittsburgh Public Schools (PPS) and all municipalities budget on a calendar-year basis. In 2024 millage increased in 25 municipalities, decreased in six municipalities and stayed the same for the county, PPS and 97 municipalities.

On the matter of assessment litigation, there were several developments this month. Two involve the common level ratio (CLR) used in assessment appeals. On Sept. 3, Common Pleas Court permitted the use of a neighborhood-centered CLR, or the “common law method,” rather than the State Tax Equalization Board (STEB) CLR. This issue was raised in a case over an assessment appeal filed in 2021.

On Sept. 27, a status report is due in Commonwealth Court on objections to STEB’s recalculation of the 2020 CLR as part of the lawsuit filed over the county’s coding of sales used in the calculation of the CLR. That same day, arguments over preliminary objections in the PPS lawsuit seeking a court-ordered reassessment are to be heard in Common Pleas Court.

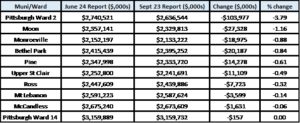

Data since the last ordinance was signed show what is happening with assessed values and county property tax collections. The Office of Property Assessments’ report on parcel counts and values from June 24 shows $84.85 billion in taxable value countywide. The Sept. 23 report shows taxable value of $84.39 billion, a decrease of $456.3 million (0.54 percent).

Two wards of the City of Pittsburgh and eight municipalities each had at least $2 billion in taxable value as of the June 24 report. In total this group represents around 30 percent of taxable value countywide. As a group, assessed value fell from $25.1 billion to $24.9 billion, a decrease of $209 million (0.83 percent). Within the group Pittsburgh Ward 14 (Squirrel Hill/Point Breeze/Frick Park) and McCandless showed minimal change over the past three months. Monroeville and Moon exceeded the average, but none compared to the decrease in Pittsburgh Ward 2 (Downtown/Part of Lower Hill District/Strip District). With its concentration of skyscrapers and the changes in work patterns as documented in previous Policy Briefs, taxable value fell 3.79 percent in the time frame.

A significant part of the decrease in Ward 2 was BPAAR’s approved reduction in the assessed value of the BNY Mellon skyscraper for 2024 from $149.9 million to $59.7 million at its Sept. 12 meeting. Since filing an appeal in 2021, the building’s value has been reduced by BPAAR and Board of Viewers’ actions from $214 million, a decrease of $154 million (72 percent).

Changes in Municipalities/Wards with $2 billion or more in taxable value

Through June, the county collected $382.4 million in property taxes, which leaves $14.9 million from what was budgeted for 2024. That amount is almost identical to collections through June 2023. Property tax refunds total $7.9 million through June, which is $3.2 million over budget and exceeds the $1.6 million refunded in the first six months of 2023. Last year, the county refunded $10.6 million in property taxes.

As the 2025 county budget introduction approaches, what remains before the council are ordinances dealing with predetermined ratio and CLR standards, how homeowners that qualify for a property tax rebate might be treated when there is a court-ordered reassessment and adopting a statistical trigger to conduct a reassessment.

On this latter proposal, rather than reassessing every certain number of years, the county would reassess if STEB certifies that one of two measurements falls outside a specified range. This idea was received with caution and skepticism by invited experts when County Council held a public hearing on reassessments in May.

Pennsylvania permits base-year assessments that can remain for a long time. Of the 10 counties that had a reassessment go into effect between 2013 and 2019, only Philadelphia has done a second one.

Mandating a cycle—a hearing on the idea was held on possible state legislation in Allegheny County in July—would prevent long gaps between assessments and make Pennsylvania’s position as an outlier on this issue a thing of the past.