Summary: A look at the improvement of the equity investments of Pittsburgh’s pensions in 2017. There is still a long way to go for the funded ratio to reach responsible levels. The city must continue to work diligently to find ways to curb pension liability growth.

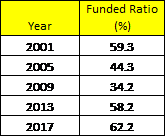

At the February meeting of Pittsburgh’s top pension officials —who are organized as a board overseeing the Comprehensive Municipal Pension Trust Fund (CMPTF)—it was announced that Pittsburgh’s pensions had achieved a funding ratio (actuarial assets divided by actuarial liabilities, for Pittsburgh $749 million and $1.2 billion, respectively) of 62.2 percent, its highest level in a long while. In 2001 the ratio stood at 59.3 percent but fell for the next several years to reach the mid-30 percent range by the end of the decade.

The CMPTF was created in 1988 to unify the investments of three plans that currently cover more than 7,400 active and inactive police, fire and non-uniformed employees. The investments “are assigned to professional asset managers that specialize in certain types of investments with oversight by an outside investment consultant and the Board in order to achieve an appropriate, diversified and balanced asset class mix to minimize portfolio risk,” according to the 2016 annual report and audit on the CMPTF. That is in line with an April 2017 study by the Pew Trusts on state and local pension investments that found most public pension systems invest in a variety of equity and fixed-income instruments offering low and high risks.

Pittsburgh Pension Funded Ratio

The CMPTF assets are composed of the invested portfolio that tries to target 60 percent equities (currently U.S., non-U.S., some hedge funds and private) and 40 percent fixed income (cash, some hedge funds, and real estate). In addition to the invested portfolio, pension funds include the stream of parking tax revenue through 2041. Bear in mind that most of the jump in funded ratio from 2009 to 2013 was the result of the city pledging parking taxes to the pension plans (a total of $735 million in annual payments). This was done to avoid having the management of the pension plans taken over by the Pennsylvania Municipal Retirement System per the requirements of Act 44 of 2009 wherein the funded ratio had to reach 50 percent or greater by Jan.1, 2011. Beginning in 2018 the city’s annual parking tax commitment is to double to $26 million.

At the end of 2017 the performance report submitted to the CMPTF placed the asset value of the pledged parking tax revenue at $301.8 million as a supplement to the $448.9 million in the invested portfolio. Thus, the parking tax pledge amounts to 40 percent of pension fund assets.

In the period from Dec. 31, 2016 to Dec. 31, 2017, the invested portfolio increased in value by 11 percent, from $403.1 million to stand at $448.9 million. That was better than the previous year-to-year increase of 7 percent.

The majority of the invested portfolio is in U.S. and non-U.S. equities. The overall change in the U.S. equities group was $16.2 million (10 percent), from $155.2 million to $171.4 million. There are five main funds in the U.S. equities grouping including the large S&P 500 Index Fund that grew 14 percent from $93.3 million to $106.1 million over the time frame. Note that the S&P Index grew 19 percent in calendar year 2017, up from 9.5 percent in 2016. Thus, the Pittsburgh pension holdings in the Index fund grew less than the Index itself. Was some money withdrawn from the fund to cover cash needs? The four other funds (Frontier Capital Management, Guyasuta Investment, Twin Capital, and CIM) increased anywhere from a high of 25 percent to a low of 1 percent.

In non-U.S. equities there are four funds (however one did not exist in December 2016 so the time frame measurement covers three funds), all of which had double-digit growth of anywhere from 23 percent to 36 percent. MFS International Fund, the largest of the three in terms of dollars, grew 23 percent. SSgA active Emerging Markets and ABS Emerging Markets grew 36 percent and 28 percent, respectively. In total, the value non-U.S. equities group grew from $69.1 million to $88.8 million.

Board members at the most recent meeting were celebrating the good returns and the improved funded ratio but are probably cautious knowing that markets can fluctuate. In 2015 the city’s finance director (a CMPTF board member) stated “We’re at the whim of the market just like any other investor.” In 2017, the same official stated “We still need to be cautious for the future because any decline in the stock market would probably pull down that funded ratio.” For the time being, however, the investment news is good.

It is easy to see why investment performance is critical. A 2009 report by the Employment Benefits Research Institute found that in many of the years from 1997 to 2007 investment earnings provided 70 percent or more of the average public pension plan’s funding.

Based on the levels of distress created by Act 44, Pittsburgh remains in moderate distress, a status assigned to municipalities with funded ratios for their pension plans in the range of 50 to 69 percent. The city was in the severe distress level initially. Getting to minimal or no distress—a funded ratio of 70 percent or higher—will almost certainly require reform of pension benefits. The city recently passed an ordinance prohibiting pension benefit enhancements such as changes to eligibility, vesting time, or service increments. This would also include getting the state to amend existing law to allow defined contribution plans for new hires and reducing the number of people on the payroll.

Using the recent boost in pension asset value due to increasing equity prices and other investment gains as an excuse not to adopt long term measures that reduce the growth in pension liabilities would be a tragic mistake.